At the 2025 Indonesia Mining Conference & Critical Metals Conference - Aluminum Industry Forum, Duncan Hobbs, Director of Industry Research at Concord Resources, shared insights on the topic of "Aluminum Market Preview."

Recent Review of the Aluminum Market

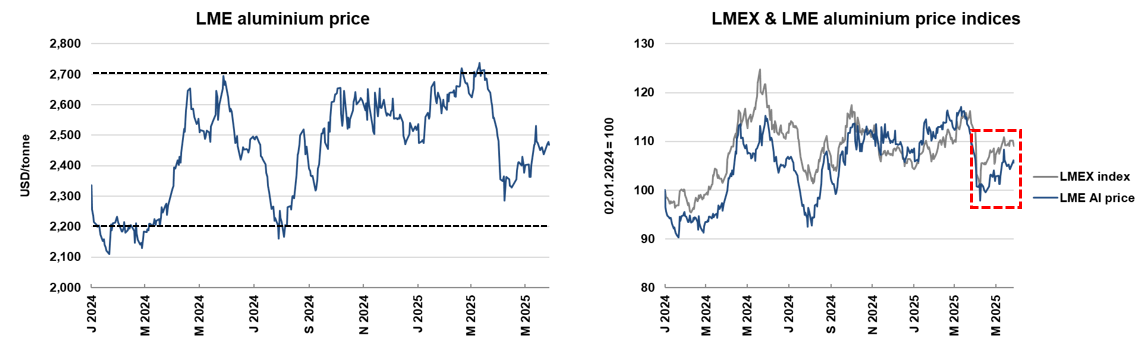

Aluminum prices on the London Metal Exchange (LME) have recently remained within a relatively stable range, though underperforming the broader market.

Since the beginning of 2024, LME spot aluminum prices have fluctuated between $2,200 and $2,700 per mt.

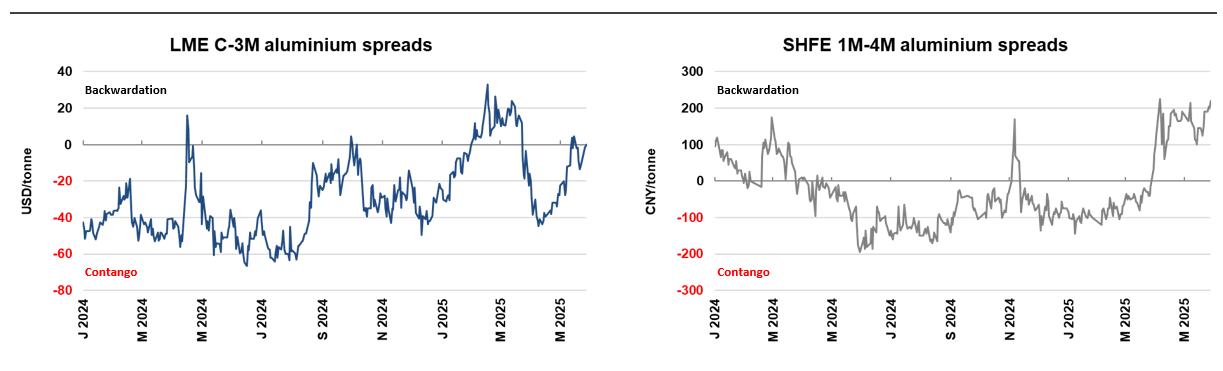

Recently, the price spread between the near-month aluminum contracts on the LME and the Shanghai Futures Exchange (SHFE) has narrowed.

Since the start of 2025, the average price spread for three-month aluminum contracts on the LME has been 8¢, compared to an average of 38¢ in 2024, marking the largest spread since 2013. Meanwhile, the aluminum price spread on the SHFE from January to April 2025 was 46 yuan, compared to just 21 yuan during the same period last year.

The weaker price spread indicates less urgent demand for aluminum metal recently, while backwardation reflects the opposite market signal.

In terms of current spot aluminum premiums across regions, compared to the end of 2024, aluminum premiums in Europe and Asia have declined, with most regions maintaining a supply surplus in the spot aluminum market. However, the US market has seen a deviation in supply and demand due to tariff issues—on June 3, 2025, local time, US President Trump signed an executive order raising tariffs on imported steel, aluminum, and their derivative products from 25% to 50%, with the tariff policy taking effect at 00:01 AM Eastern Time on June 4, leading to an increase in spot aluminum premiums.

Over the past year, visible aluminum metal inventories have decreased, with current inventory levels falling to a very low level compared to market size. Currently, the combined latest inventories on the London Metal Exchange (LME) and the Shanghai Futures Exchange (SHFE) total approximately 500,000 mt, a YoY decline of over 60%. This inventory level can only meet about 2.5 days of global consumption, whereas a decade ago, it could support 25 days of consumption.

Recent Commentary on the Aluminum Market

Global aluminum consumption reached a new record last year, though the growth rate has slowed. In 2024, global aluminum consumption is expected to reach approximately 73 million mt, a 4% increase from the previous year and more than double the figure from two decades ago.

However, since the outbreak of COVID-19, the average annual growth rate of global aluminum consumption has been below 2%, while the compound annual growth rate from 2005 to 2024 exceeded 4%.

The latest aluminum market assessment indicates that China has played a major role in the long-term growth of aluminum consumption, with some aluminum products also flowing into the international market. From 2004 to 2024, China's aluminum consumption surged more than sevenfold, reaching 45 million mt, accounting for over 90% of global total consumption. Meanwhile, China's exports of aluminum semi-finished products and certain finished products increased more than twelvefold over this period, reaching 8.5 million mt.

Chinese Market Dynamics: China's aluminum production has recently risen significantly, though it is approaching the upper limit set by the government. From 2004 to 2024, China's aluminum production increased more than sixfold, reaching approximately 44 million mt/year by 2025, accounting for 98% of the government-set upper limit.

Other Regions Globally: In contrast to China's rapid growth, aluminum production in Europe and North America has shown a long-term downward trend. Meanwhile, the Gulf Cooperation Council countries and Asian countries outside China have significantly increased their aluminum production.

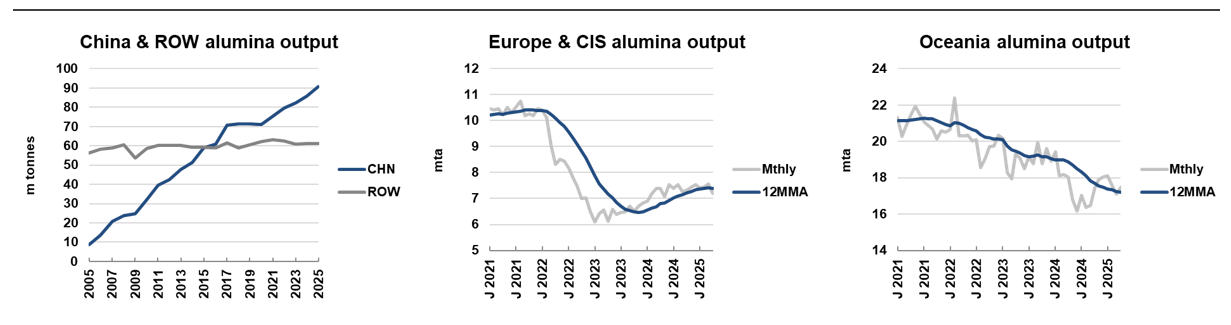

Alumina Market:

It is reported that the regional distribution of alumina production is undergoing significant changes. China's alumina production continues to climb, while production in Europe and Oceania has shown a recent downward trend.

Over the past two decades, China's alumina production has surged nearly tenfold and is expected to account for 58% of global total production by 2024. In contrast, production in other regions has remained largely stable over the past fifteen years. However, China's alumina refining capacity and its expansion are highly dependent on coal energy, a reliance that may have unsustainable environmental impacts in the long run.

Since the outbreak of the Russia-Ukraine conflict, alumina production in Europe and CIS countries has declined sharply due to soaring costs; at the same time, production in Oceania has also decreased due to operational issues.

Guinea has now become the world's largest bauxite producer, supplying a significant amount of imported bauxite to China. In 2024, Guinea's bauxite production will reach approximately 135 million mt, accounting for about 35% of global total production. This figure marks that Guinea surpassed Australia in bauxite production in 2023 and overtook China in 2022.

Over the past five years, Guinea's bauxite exports to China have increased more than 2.5 times. By April 2025, the twelve-month moving average of imports will reach approximately 125 million mt/year, accounting for over 70% of China's total imports.

Currently, China's aluminum industry is highly dependent on Guinea for primary aluminum supply, posing significant risks to the supply chain. Additionally, the volume of Guinea's bauxite imported into China has exceeded the contribution of Australian iron ore to China's pig iron and crude steel production.

Key Macro Indicators

Inflation in the US has slowed down somewhat but has remained consistently above the target value over the past year and a half, and inflation expectations have recently risen significantly.

The US Fed's preferred inflation gauge, the Personal Consumption Expenditures Price Index (PCE), rose 2.6% YoY in March, exceeding the 2% target, while the Consumer Price Index (CPI) increased 2.3% YoY in April.

By early 2025, the MoM increases in one-year and five-year forward inflation rates reached their highest levels since the 2009 financial crisis.

Inflation in the US is crucial as it not only affects real yields but is also closely tied to commodity prices. Over the past two to three years, the correlation between the Bloomberg Commodity Index (BCOM) and real yields has strengthened significantly; higher inflation expectations correlate with higher commodity prices.

US Treasury yields and the US dollar typically move in the same direction, while the value of the US dollar is often inversely correlated with commodity prices.

However, this relationship has recently broken down, suggesting capital outflows from the US. A weaker US dollar may support commodity prices.

China currently dominates global alumina and primary aluminum production. Over the past two decades, China's share of global alumina production has increased approximately fivefold, now exceeding 60% of the world's total; primary aluminum production has followed a similar growth trajectory.

Given China's significant share of global alumina production, the USD/CNY exchange rate has a substantial impact on the global cost supply curve.

Outlook for the Aluminum Market

The pace of recovery in the global market and fluctuations in the Chinese market will significantly influence the aluminum market.

The primary driver of aluminum consumption is industrial production. Statistics show that YoY changes in industrial production explain over 75% of the annual YoY changes in aluminum consumption. Additionally, industry performance significantly impacts aluminum consumption, particularly in the transportation and construction sectors, which have a higher dependency on aluminum.

Global industrial output is expected to return to normal trend levels in 2025 after a period of weakness from 2023-2024. While accelerated industrial production may support growth in aluminum consumption, downside risks remain under the current policy environment.

Furthermore, output in the automotive and construction sectors is expected to lag behind overall industrial production, with construction growth specifically slowing in 2025 compared to 2024.

China accounts for over 60% of global aluminum consumption. However, current structural economic challenges suggest that future growth may slow down.

The real estate market is experiencing a structural decline, primarily driven by population decline and falling home prices. This situation has weakened consumer confidence and spending power.

Additionally, overcapacity in the manufacturing sector, particularly in aluminum smelting, has led to a decline in producer prices. Meanwhile, aluminum exports are also facing increasing restrictions.

Europe accounts for approximately 10% of global aluminum consumption. The market has been sluggish recently but is expected to experience a limited recovery from a low base.

In 2024, European aluminum consumption is projected to stabilize at around 7.4 million mt, close to the lowest level in a decade. This is partly attributed to the impact of rising energy prices. However, a limited recovery is expected as energy prices pull back, monetary policies ease, and more robust fiscal stimulus measures are implemented, with Southern Europe anticipated to outperform Northern Europe.

Current Status and Influencing Factors of the US Aluminum Market

The US accounts for approximately 6% of global zinc consumption and, as a major import market, is facing pressure from hefty tariffs.

Currently, the US is the world's largest aluminum metal import market, with 60%-70% of its aluminum imports coming from Canada. The high tariff policies implemented by the Trump administration may cause significant disruptions to the market. At the very least, policy uncertainty will adversely affect economic growth.

India accounts for approximately 4% of global aluminum consumption; growth is strong but slowing, and the base remains limited.

By 2024, India will become the world's third-largest zinc market, with consumption of approximately 2.5 million mt, but it will still be relatively small compared to China or even the early "super cycle" years.

Due to the foreign exchange policy of the Reserve Bank of India, monetary policy has been overly tight in recent times, and the Purchasing Managers' Index (PMI) has been declining. Additionally, there is the issue of oligopolies hindering growth.

National Policy Priorities: Energy, Inflation, and Industrial Profitability

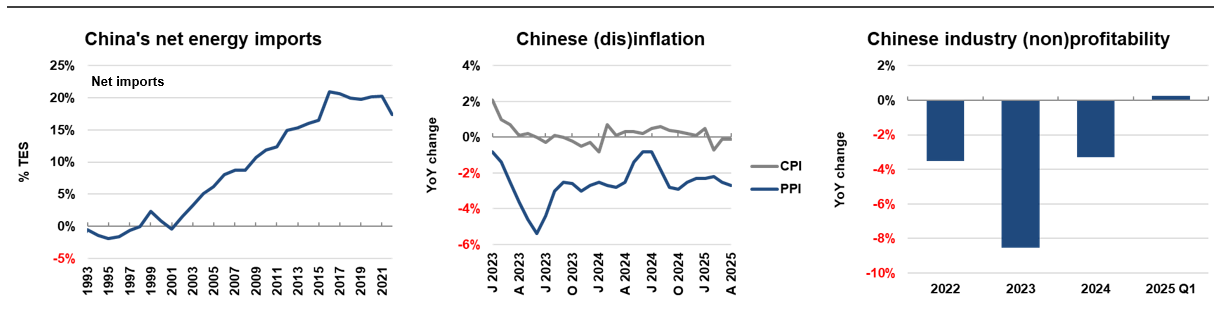

As a net energy importer, China imported 17% of its total energy consumption in 2022. Government policies aim to reduce the energy intensity of economic activities to achieve a greener economic development.

In recent years, the Consumer Price Index (CPI) has remained close to zero for two consecutive years, while the Producer Price Index (PPI) has been negative since year-end 2022. Industrial profitability has declined for three consecutive years, reflecting the phenomenon of overcapacity.

The production of aluminum and alumina is highly energy-dependent. Currently, there is a significant surplus in domestic aluminum and alumina production capacity in China, far exceeding domestic demand.

National Policy Priorities: Curbing Industrial Overcapacity

To address the issue of industrial overcapacity, the Ministry of Industry and Information Technology (MIIT) announced the "High-Quality Development Plan" for the aluminum industry for the period from 2025 to 2027 on March 28.

Bauxite:The goal is to increase bauxite production by 3% to 5% annually.

Alumina: New refining capacity enterprises should ensure they have an adequate supply of bauxite to meet factory needs. Meanwhile, the red mud recycling rate is required to reach at least 15%.

Primary aluminum: Production will be limited to approximately 45 million mt/year, with efforts focused on improving energy efficiency and actively introducing green energy.

Secondary aluminum: The target is for annual secondary aluminum production to exceed 15 million mt.

International cooperation: Enterprises are encouraged to cooperate with resource-rich countries to promote the transition from bauxite mining to primary products, thereby advancing the development of the global supply chain.

By 2025, global primary aluminum production and consumption are expected to grow synchronously at an average annual rate of approximately 2.5%, achieving a balance between market supply and demand.

In the long term, Asia will be the primary driver of aluminum production growth. In particular, Indonesia is expected to contribute approximately 40% of the global total production by 2029, leading the global aluminum market forward.

Summary

Aluminum prices have shown a volatile trend recently. Despite an abundant market supply last year, supply chain inventory remained low. Any production disruptions or unexpected increases in demand could trigger a sharp rise in aluminum prices. Currently, China's aluminum supply chain heavily relies on bauxite imports from Guinea. If the supply flow is disrupted in any way, the concentration risk of the supply chain will lead to an increase in aluminum prices.

Although US inflation has slowed down, it remains above the target level, and due to certain political risks, the relationship between the US dollar and US Treasury yields has been impaired. The US dollar exchange rate has a significant impact on the cost and supply curves of aluminum and alumina, and a depreciation of the US dollar may support an increase in aluminum prices.

Multiple regions globally are experiencing an industrial upswing, which will contribute to the synchronous growth of aluminum consumption and production by 2025. However, US policies and the manner in which they are formulated still pose risks to global economic growth. China's national policy focus is shifting towards stricter control over aluminum smelting and alumina refining capacity. Despite the bullish long-term outlook for aluminum prices, the risk of overexpansion in other regions still exists.

》Click to view the special report on the 2025 Indonesia Mining Conference & Critical Metals Conference